Definition:

COB in insurance stands for “Coordination of Benefits.”

It is a process used by insurance companies to determine which policy pays first when a person is covered by more than one health insurance plan.

Imagine this: you have health insurance through your employer, but you’re also covered under your spouse’s plan. Sounds like a great safety net, right? 🤔

But here’s the catch when a medical bill arrives, which insurance pays first? That’s where Coordination of Benefits (COB) steps in.

Understanding what COB means in insurance isn’t just helpful it can save you from claim delays, unexpected bills, and a lot of confusion. Whether you’re juggling multiple policies or just want to be prepared, this guide will break everything down in a simple, clear, and practical way.

Origin and Purpose of COB in Insurance

Where Did COB Come From?

The concept of Coordination of Benefits was introduced as health insurance became more widespread, especially in workplaces where dual coverage became common (e.g., spouses both having employer-sponsored plans).

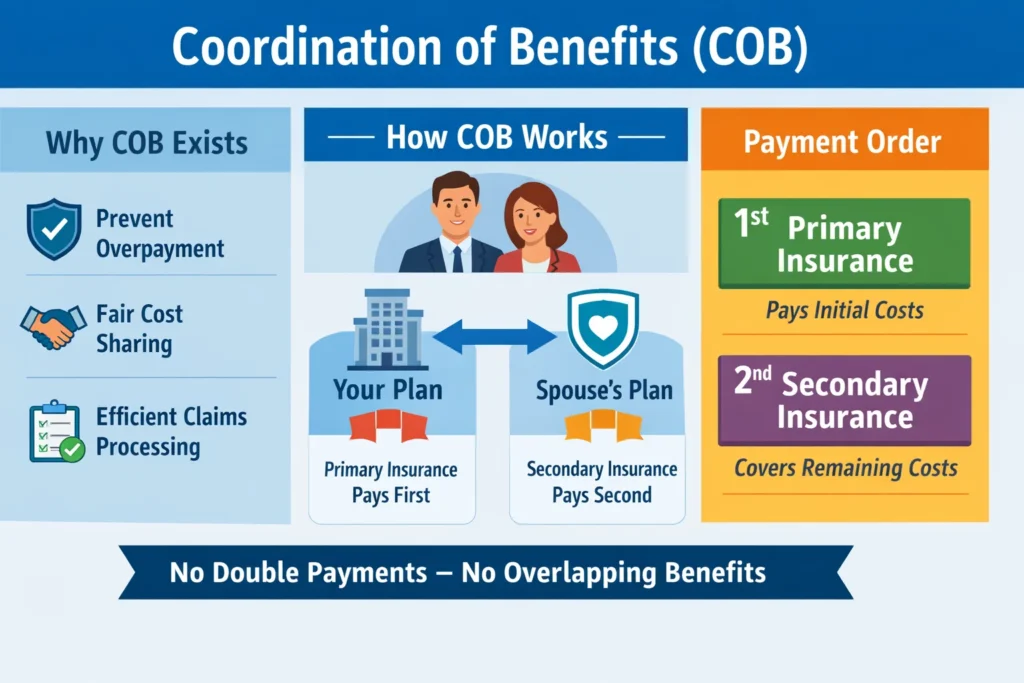

Insurance companies needed a standardized system to:

- Prevent overpayment

- Avoid fraud or duplicate claims

- Clearly define payment responsibility

Why COB Exists

COB ensures:

- You don’t get paid more than your medical bill

- Insurance companies share costs fairly

- Claims are processed efficiently

The Core Idea

Without COB, someone with two insurance plans could technically receive double reimbursement which isn’t allowed. COB prevents this by assigning:

- Primary insurance (pays first)

- Secondary insurance (pays remaining costs, if applicable)

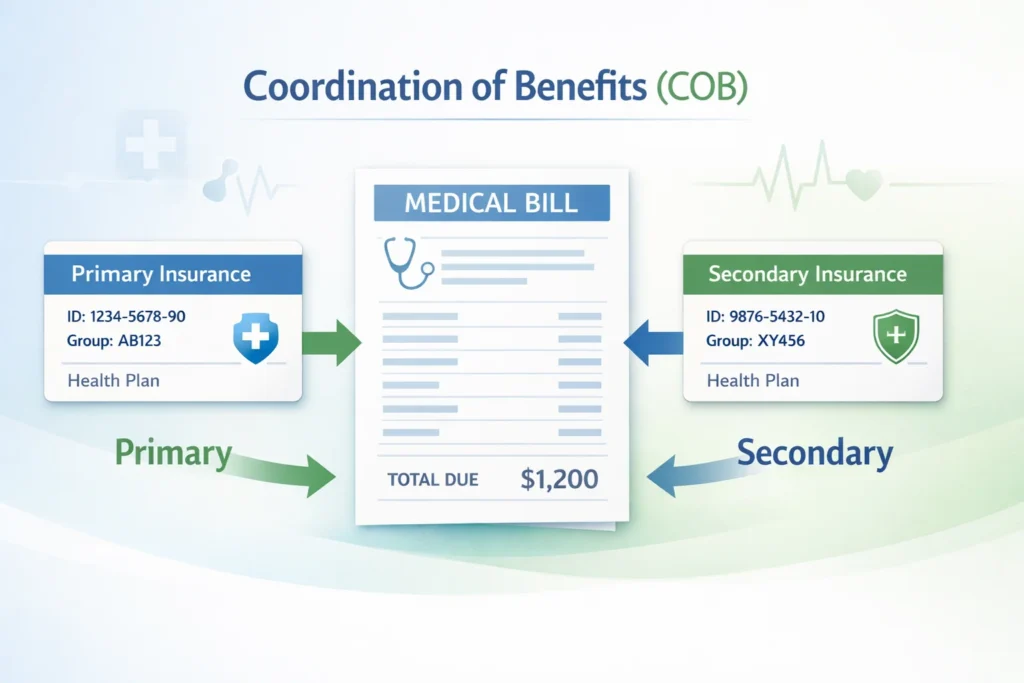

How COB Works in Real Life

Here’s a simple breakdown of how Coordination of Benefits functions:

- You receive medical treatment.

- The bill is sent to your primary insurance.

- Primary insurance pays its portion.

- The remaining balance goes to your secondary insurance.

- Secondary insurance may cover part or all of the remaining amount.

Example Scenario

Let’s say:

- Your medical bill = $1,000

- Primary insurance pays = $700

- Remaining = $300

Now:

- Secondary insurance may pay the $300 (fully or partially)

Example Table: How COB Applies

| Scenario | Primary Insurance | Secondary Insurance | Outcome |

|---|---|---|---|

| Employee + Spouse Plan | Employee’s plan | Spouse’s plan | Employee plan pays first |

| Child with Two Parents | Parent with earlier birthday (birthday rule) | Other parent | Birthday rule determines primary |

| Active Employee + Retiree Plan | Active employee plan | Retiree plan | Active plan pays first |

| Medicaid + Private Insurance | Private insurance | Medicaid | Medicaid pays last |

Rules That Determine Primary vs Secondary Insurance

Insurance companies follow standard COB rules:

1. The Birthday Rule 🎂

For children covered under both parents:

- The parent whose birthday (month/day) comes first in the year has the primary plan

2. Employment Status Rule

- Active employee coverage is primary

- Retiree or inactive coverage is secondary

3. Length of Coverage Rule

- The plan you’ve had longer may be primary

4. Court Orders

- In some cases (e.g., divorce), a legal agreement determines responsibility

Real-World Usage of COB

Friendly Tone 🙂

“Don’t worry! Your secondary insurance should cover most of what’s left after your primary plan pays.”

Neutral/Professional Tone

“According to COB guidelines, your employer-sponsored plan will act as the primary payer.”

Negative/Dismissive Tone 😐

“Your claim was delayed because COB information was incomplete. Please update your insurance details.”

Common Situations Where COB Applies

You’ll encounter COB if you:

- Have insurance through two jobs

- Are covered under your spouse’s plan

- Have Medicare + private insurance

- Have Medicaid + employer insurance

- Are a dependent child with dual coverage

COB vs Related Insurance Terms

Understanding COB becomes easier when you compare it with similar concepts:

Difference COB vs Primary Insurance

| Term | Meaning |

|---|---|

| COB | Process of deciding payment order |

| Primary Insurance | Pays first |

Comparing COB vs Secondary Insurance

| Term | Meaning |

|---|---|

| COB | Determines payment order |

| Secondary Insurance | Pays after primary |

COB vs Deductible

| Term | Meaning |

|---|---|

| COB | Coordination between insurers |

| Deductible | Amount you pay before insurance kicks in |

COB vs Copayment

| Term | Meaning |

|---|---|

| COB | Payment coordination system |

| Copayment | Fixed amount you pay per service |

Alternate Meanings of “COB”

While COB in insurance means Coordination of Benefits, the abbreviation can have other meanings in different contexts:

- Close of Business (commonly used in emails)

- Corn on the Cob 🌽 (informal)

- Cash on Board (finance/logistics context)

👉 Important: Always use context to understand the meaning correctly.

Practical Tips for Handling COB Smoothly

Here’s how to avoid headaches:

✔️ Keep Your Insurance Info Updated

Always inform both insurers about:

- Other coverage

- Changes in employment

- Family status updates

✔️ Respond to COB Questionnaires

Insurance companies may send forms asking about other coverage don’t ignore them!

✔️ Understand Your Plans

Know:

- Which is primary

- What each covers

✔️ Track Your Claims

Monitor:

- Payments

- Remaining balances

- Claim status

✔️ Communicate with Providers

Let doctors and hospitals know you have multiple insurance plans.

Polite or Professional Alternatives to “COB”

Instead of using the abbreviation, you can say:

- “Coordination of Benefits process”

- “Insurance payment coordination”

- “Multiple insurance coverage arrangement”

These alternatives are especially useful in formal communication or when speaking with someone unfamiliar with insurance jargon.

Common Mistakes People Make with COB

Avoid these pitfalls:

- ❌ Not informing insurers about dual coverage

- ❌ Assuming both plans will pay fully

- ❌ Ignoring COB requests or forms

- ❌ Confusing primary and secondary roles

- ❌ Expecting reimbursement beyond total cost

FAQs

1. What does COB mean in health insurance?

COB stands for Coordination of Benefits, which determines which insurance pays first when you have multiple plans.

2. Why is COB important?

It prevents duplicate payments and ensures claims are processed correctly between insurers.

3. How do I know which insurance is primary?

It depends on rules like employment status, the birthday rule, or plan type.

4. Can both insurance plans pay 100%?

No. Combined payments cannot exceed the total cost of the service.

5. What happens if I don’t complete COB information?

Your claims may be delayed or denied until the information is provided.

6. Does COB apply to dental and vision insurance?

Yes, COB rules can apply to dental, vision, and other types of insurance as well.

7. Is COB the same as dual coverage?

Not exactly. Dual coverage means you have two plans; COB is the system that manages how they pay.

8. Can COB save me money?

Yes, secondary insurance may reduce your out-of-pocket costs.

Conclusion:

Coordination of Benefits might sound complicated at first, but it’s actually a straightforward system once you understand the basics.

Remember:

- COB decides who pays first

- It applies when you have multiple insurance plans

- It prevents overpayment and confusion

- Following COB rules helps avoid claim delays

Final Tip 💡

Always keep your insurance providers informed and stay proactive. A little awareness about COB can save you time, stress, and money in the long run.

Discover More Related Articles:

- Unhinged Meaning | Pop Culture & Memes In 2026

- AWOL Meaning | Why Someone Suddenly Disappears Online In 2026

Jessica Brown is a language-focused writer who creates well-researched articles on word meanings, abbreviations, and everyday expressions. She contributes to meanvoro.com, delivering simple, reliable, and reader-friendly content designed to make complex terms easy to understand.