Cash value in life insurance is the savings component of certain permanent life insurance policies that grows over time and can be accessed by the policyholder during their lifetime. It accumulates on a tax-deferred basis and can be used through withdrawals, loans, or policy surrender.

Life insurance is often thought of as a way to financially protect loved ones after death. While that is true, some types of life insurance offer more than just a death benefit. Cash value life insurance combines protection with a built-in savings element.

This cash value can grow over time and provide financial flexibility while you are still alive. Policyholders may use it to cover emergencies, supplement retirement income, or help pay premiums later in life. However, it also comes with costs, rules, and long-term considerations that are important to understand.

Understanding cash value is important if you are comparing life insurance options or planning long-term financial protection. It is one of the key features that separates permanent life insurance from term life insurance.

Origin and Background of Cash Value Life Insurance

Cash value life insurance became popular as insurers designed policies that served both insurance and savings purposes. Permanent life insurance products such as whole life and universal life were created to offer:

- Lifetime coverage

- Guaranteed or variable growth

- A savings component tied to premiums

Over time, cash value became a major selling point, especially for individuals seeking long-term financial planning tools rather than temporary coverage.

What Is Cash Value in Life Insurance?

Cash value is a portion of your premium that is set aside and invested by the insurance company. This value grows gradually based on the policy type and terms.

Key Characteristics of Cash Value

| Feature | Explanation |

|---|---|

| Accumulates over time | Grows slowly in early years, faster later |

| Tax-deferred growth | Taxes are not due while funds remain in the policy |

| Accessible during lifetime | Can be borrowed or withdrawn |

| Reduces death benefit if used | Loans or withdrawals may lower payout |

Types of Life Insurance With Cash Value

Not all life insurance policies include cash value. It is only found in permanent life insurance.

| Policy Type | Cash Value Included | Growth Style |

|---|---|---|

| Whole Life Insurance | Yes | Guaranteed growth |

| Universal Life Insurance | Yes | Interest-based, flexible |

| Variable Life Insurance | Yes | Market-based, higher risk |

| Term Life Insurance | No | No savings component |

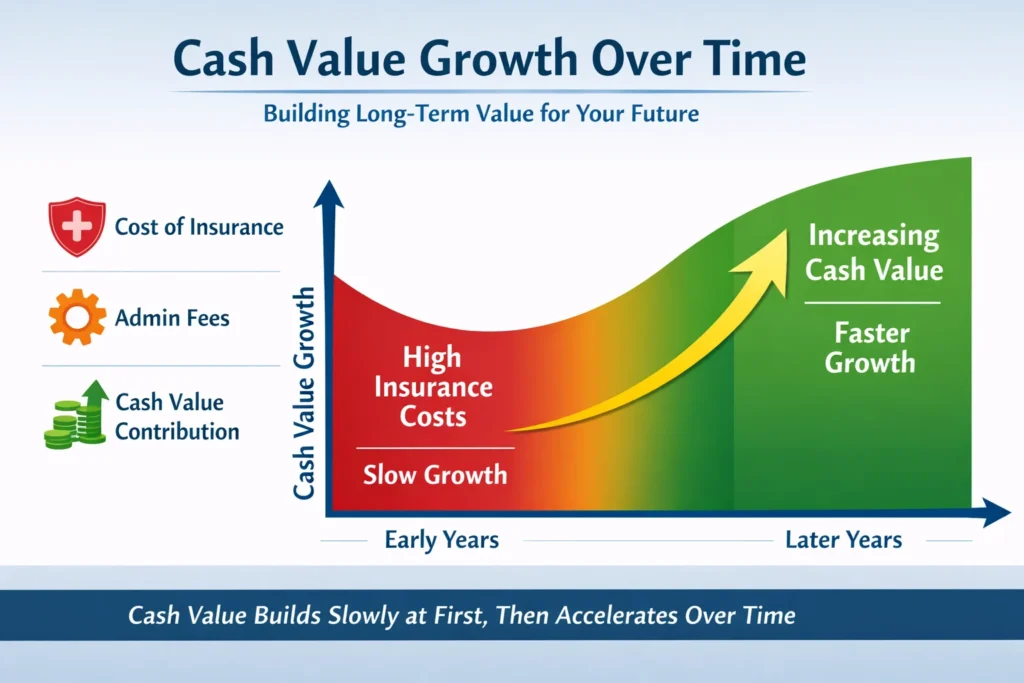

How Cash Value Builds Over Time

When you pay your premium, it is divided into three parts:

- Cost of insurance

- Administrative fees

- Cash value contribution

In the early years, most of your premium goes toward insurance costs. Over time, a larger portion contributes to cash value growth.

Important note: Cash value growth is slow at first. These policies are designed for long-term use, not short-term savings.

How You Can Use Cash Value

Cash value provides flexibility, but it must be used carefully.

Common Ways to Access Cash Value

| Method | Description | Impact |

|---|---|---|

| Policy loan | Borrow against cash value | Reduces death benefit if unpaid |

| Withdrawal | Take money out | Permanently lowers policy value |

| Premium payments | Use cash value to pay premiums | Keeps policy active |

| Policy surrender | Cancel policy for cash | Ends coverage |

Real-Life Examples of Cash Value Usage

| Scenario | Example | Outcome |

|---|---|---|

| Emergency expense | Policyholder borrows from cash value | Coverage stays active |

| Retirement income | Uses withdrawals gradually | Reduced death benefit |

| Job loss | Uses cash value to pay premiums | Avoids policy lapse |

| Full surrender | Cancels policy for lump sum | Coverage ends |

Cash Value vs Death Benefit

Many people confuse cash value with the death benefit. They are not the same.

| Feature | Cash Value | Death Benefit |

|---|---|---|

| Available while alive | Yes | No |

| Paid to beneficiaries | No | Yes |

| Affected by loans | Yes | Yes |

| Main purpose | Savings | Protection |

In most cases, beneficiaries receive only the death benefit, not both the death benefit and cash value.

Advantages of Cash Value Life Insurance

- Lifetime coverage

- Tax-deferred growth

- Access to funds without strict approval

- Can support long-term financial planning

Disadvantages and Considerations

- Higher premiums than term life

- Slow growth in early years

- Fees and administrative costs

- Misuse can reduce or eliminate death benefit

Cash value life insurance is best suited for those who can commit long-term and afford higher premiums.

Polite and Professional Alternatives to Saying “Cash Value”

In professional or consumer-friendly communication, insurers may use different wording.

| Term | Meaning |

|---|---|

| Policy value | Total accumulated value |

| Savings component | Informal explanation |

| Accumulated value | Formal documentation |

| Surrender value | Amount paid if policy is canceled |

FAQs

- What does cash value mean in life insurance?

It is the savings portion of a permanent life insurance policy that grows over time. - Do all life insurance policies have cash value?

No, only permanent life insurance policies include cash value. - Can I withdraw my cash value anytime?

Yes, but withdrawals may reduce your death benefit. - Is cash value taxable?

Growth is tax-deferred, but withdrawals beyond premiums paid may be taxed. - What happens to cash value when I die?

Typically, it is absorbed by the insurer and not paid to beneficiaries. - Is cash value a good investment?

It is generally conservative and designed for stability, not high returns. - Can cash value pay my premiums?

Yes, many policies allow premiums to be paid using accumulated cash value. - Is cash value better than term life insurance?

It depends on your goals, budget, and long-term financial plans.

Practical Tips for Using Cash Value Wisely

- Review policy illustrations carefully

- Avoid excessive borrowing early on

- Understand fees and surrender charges

- Use cash value as a long-term strategy

- Consult a licensed insurance professional

Conclusion

Cash value in life insurance adds a savings element to lifelong protection. While it offers flexibility, tax advantages, and long-term benefits, it also requires commitment and understanding.

- Pro tip: These policies work best when held long-term.

- Smart approach: Align cash value life insurance with your broader financial goals.

When used correctly, cash value life insurance can be a powerful tool for both protection and financial planning.

Discover More Related Articles:

- JOI Mean in Porn | Understanding the Adult Content Slang Term In 2026

- The Root Tele Mean in Television | Understanding the Word’s Origin In 2026

- Closed Circle Mean in Math |The Symbol Most Students Misunderstand In 2026

Ryan Thompson is an experienced content writer specializing in slang terms, texting abbreviations, and word meanings. He writes for meanvoro.com, where he creates accurate and easy-to-understand language content for readers.