Underwriting in insurance is the process insurers use to evaluate risk before approving a policy. It involves reviewing an applicant’s information to decide whether to provide coverage, what terms to offer, and how much the premium should be.

Insurance is all about risk. Before an insurance company agrees to cover a person, vehicle, home, or business, it needs to understand how risky that coverage might be. That’s where underwriting comes in.

Underwriting helps insurance companies stay financially stable while ensuring customers are charged fair and appropriate premiums. Without underwriting, insurers wouldn’t be able to balance protection for customers with long-term sustainability.

In this article, you’ll learn what underwriting means, how it works, who performs it, and how it affects insurance approval and pricing.

If you’ve ever applied for insurance and been asked detailed questions about health, property, driving history, or finances, you’ve already experienced underwriting. It’s one of the most important steps in the insurance process, even though it often happens behind the scenes.

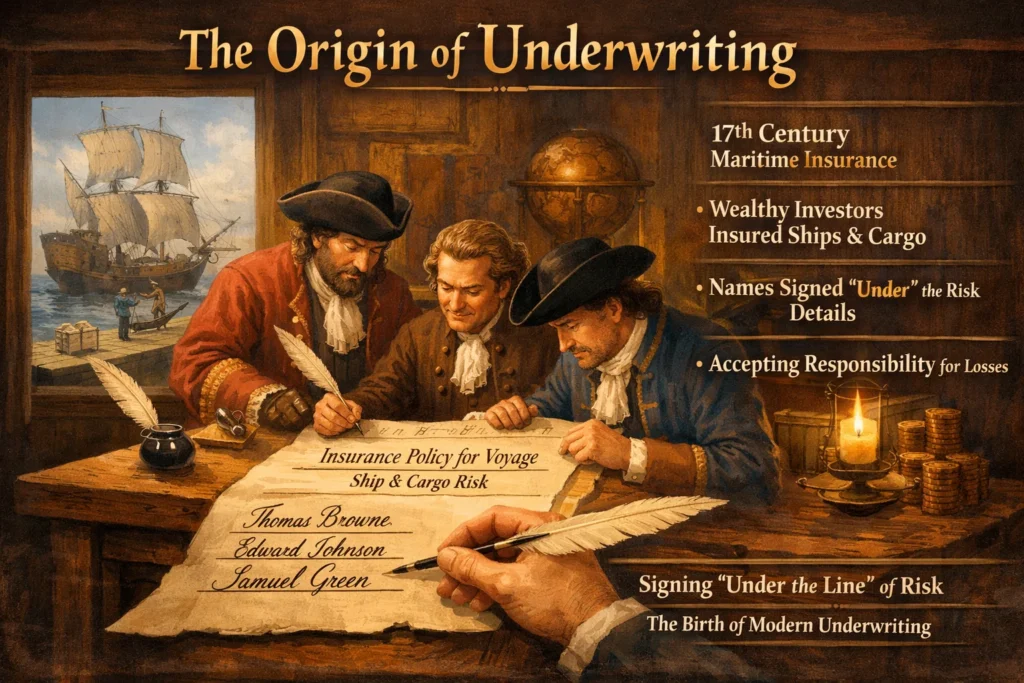

Origin of the Term “Underwriting”

The term underwriting dates back to the 17th century in maritime insurance.

- Wealthy individuals would agree to insure ships and cargo

- They wrote their names under the description of the risk

- Their signature meant they accepted responsibility for part of the loss

Over time, this practice evolved into the modern underwriting process used across all types of insurance today.

What Is the Purpose of Underwriting?

Underwriting exists to answer three key questions:

- Should this risk be insured?

- Under what conditions should coverage be offered?

- How much should the policy cost?

By analyzing risk carefully, insurers can:

- Prevent excessive losses

- Offer fair pricing

- Customize coverage terms

- Protect both the company and policyholders

How the Underwriting Process Works

While details vary by insurance type, the underwriting process generally follows these steps:

- Application Review

The insurer collects information from the applicant. - Risk Evaluation

Data is analyzed to assess the likelihood of a claim. - Risk Classification

The applicant is placed into a risk category. - Decision Making

Coverage is approved, modified, or denied. - Premium Determination

Pricing is set based on the level of risk.

What Information Do Underwriters Review?

Underwriters examine different factors depending on the type of insurance.

Common Factors Considered

| Insurance Type | Information Reviewed |

|---|---|

| Health Insurance | Medical history, age, lifestyle |

| Life Insurance | Age, health records, occupation |

| Auto Insurance | Driving record, vehicle type |

| Home Insurance | Property condition, location |

| Business Insurance | Industry risk, revenue, claims history |

The goal is always the same: predict future risk as accurately as possible.

Examples of Underwriting in Real Life

Example Table

| Scenario | Underwriting Decision | Reason |

|---|---|---|

| Healthy applicant applies for life insurance | Approved at low premium | Low health risk |

| Driver with multiple accidents | Approved with higher premium | Higher claim likelihood |

| Home in flood-prone area | Coverage limited or adjusted | Environmental risk |

| Business with no prior claims | Approved with favorable terms | Strong risk profile |

These decisions help insurers balance coverage availability with financial responsibility.

Types of Insurance Underwriting

1. Automated Underwriting

Uses algorithms and data systems to make quick decisions.

Common for auto and basic health policies.

2. Manual Underwriting

A human underwriter reviews the application in detail.

Common for life, business, and complex policies.

3. Reinsurance Underwriting

Used when insurers transfer part of the risk to another insurer.

Underwriting vs Claims vs Actuarial Work

| Role | Purpose | Timing |

|---|---|---|

| Underwriting | Assess risk before coverage | Before policy starts |

| Claims | Handle losses and payouts | After an incident |

| Actuarial | Analyze data and pricing models | Long-term planning |

Each role supports the insurance system in a different way.

Can Underwriting Affect Policy Approval?

Yes. Underwriting outcomes usually fall into one of these categories:

- Approved as applied

- Approved with higher premium

- Approved with exclusions or limits

- Postponed for more information

- Declined

A denial does not always mean permanent rejection. Conditions may change over time.

Polite and Professional Ways to Explain Underwriting

When explaining underwriting to customers or clients:

- “Underwriting helps determine the right coverage and pricing.”

- “It’s a standard review process to assess risk fairly.”

- “This step ensures your policy fits your situation.”

Clear explanations help reduce confusion and build trust.

Common Misconceptions About Underwriting

- It’s not meant to reject people unfairly

- It doesn’t always raise prices

- It applies to almost all insurance types

- It’s not the same as claims processing

Understanding this prevents unnecessary frustration during applications.

FAQs

- What does underwriting mean in insurance?

It’s the process of evaluating risk before approving coverage. - Who performs underwriting?

Trained professionals called underwriters, sometimes supported by automated systems. - Does underwriting happen for every policy?

Yes, though some simple policies use automated underwriting. - How long does underwriting take?

It can take minutes for automated reviews or weeks for complex cases. - Can underwriting increase my premium?

Yes, higher risk usually means higher cost. - Is underwriting required for renewals?

Often yes, especially if circumstances have changed. - Can underwriting deny coverage?

Yes, if the risk is too high. - Can I appeal an underwriting decision?

In many cases, yes, especially with additional information.

Practical Tips for Applicants

- Provide accurate and complete information

- Ask questions if terms are unclear

- Understand that underwriting protects both sides

- Improve risk factors where possible

- Keep documentation organized

Conclusion

Underwriting is the backbone of the insurance industry. It ensures that coverage decisions are fair, premiums are accurate, and insurers can meet their financial obligations. While it may feel complex, underwriting ultimately protects both policyholders and insurance companies.

Knowing how underwriting works empowers you to make better insurance decisions and navigate policies with confidence.

Discover More Related Articles:

- JOI Mean in Porn | Understanding the Adult Content Slang Term In 2026

- The Root Tele Mean in Television | Understanding the Word’s Origin In 2026

- Closed Circle Mean in Math |The Symbol Most Students Misunderstand In 2026

Madison Taylor is an experienced content writer who focuses on researching and explaining word meanings, slang, and texting terms. She writes for meanvoro.com, creating clear and accurate to help readers understand language easily.